The Pendulum Swings Back

Monthly Commentary | May 5, 2026

Monthly Market Summary

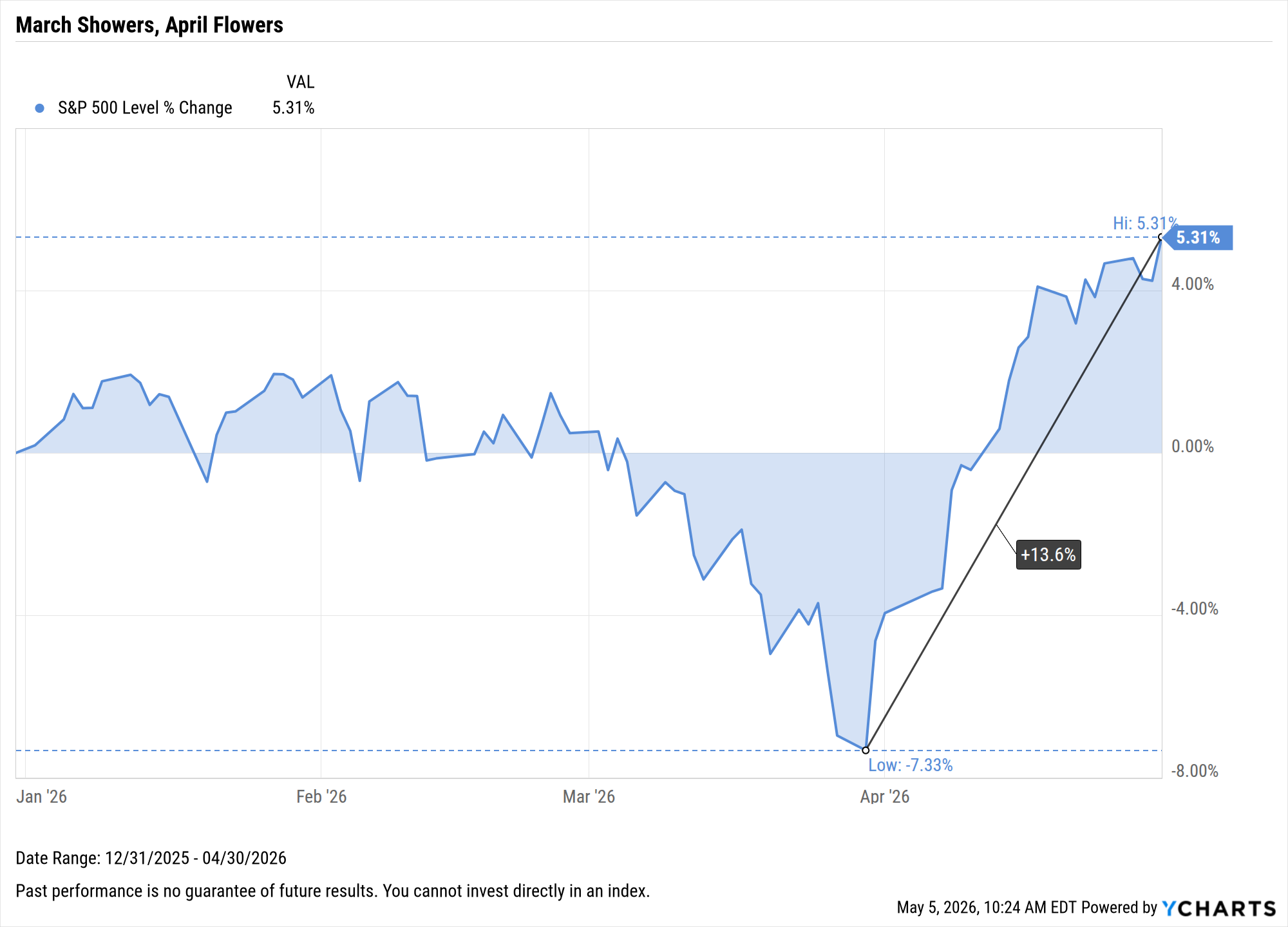

April 2026: The Strongest Month in Nearly Six Years

Throughout a difficult first quarter, our message was steady: stay the course. Setbacks are the price long-term investors pay for the returns equities have delivered over decades. April delivered the proof. The S&P 500 delivered a total return of 10.5 percent — its strongest single-month return since November 2020 — and recovered nearly all of the first quarter’s loss. Investors who held their diversified portfolios through the volatility were rewarded. Those who sold near the March lows were not. The Iran conflict, the tariff regime, and the questions surrounding the AI investment cycle have not been fully resolved, and they may not be for some time. That is the nature of equity investing. Markets do not wait for clarity to recover, and the best months arrive without an invitation. April was such a month.

• S&P 500: The S&P 500 advanced approximately 10.5 percent in April, its strongest single-month return since November 2020, and turned positive for the year with a year-to-date gain of approximately 5.7 percent. The index set a new all-time closing high on April 24 after a 13-day winning streak.

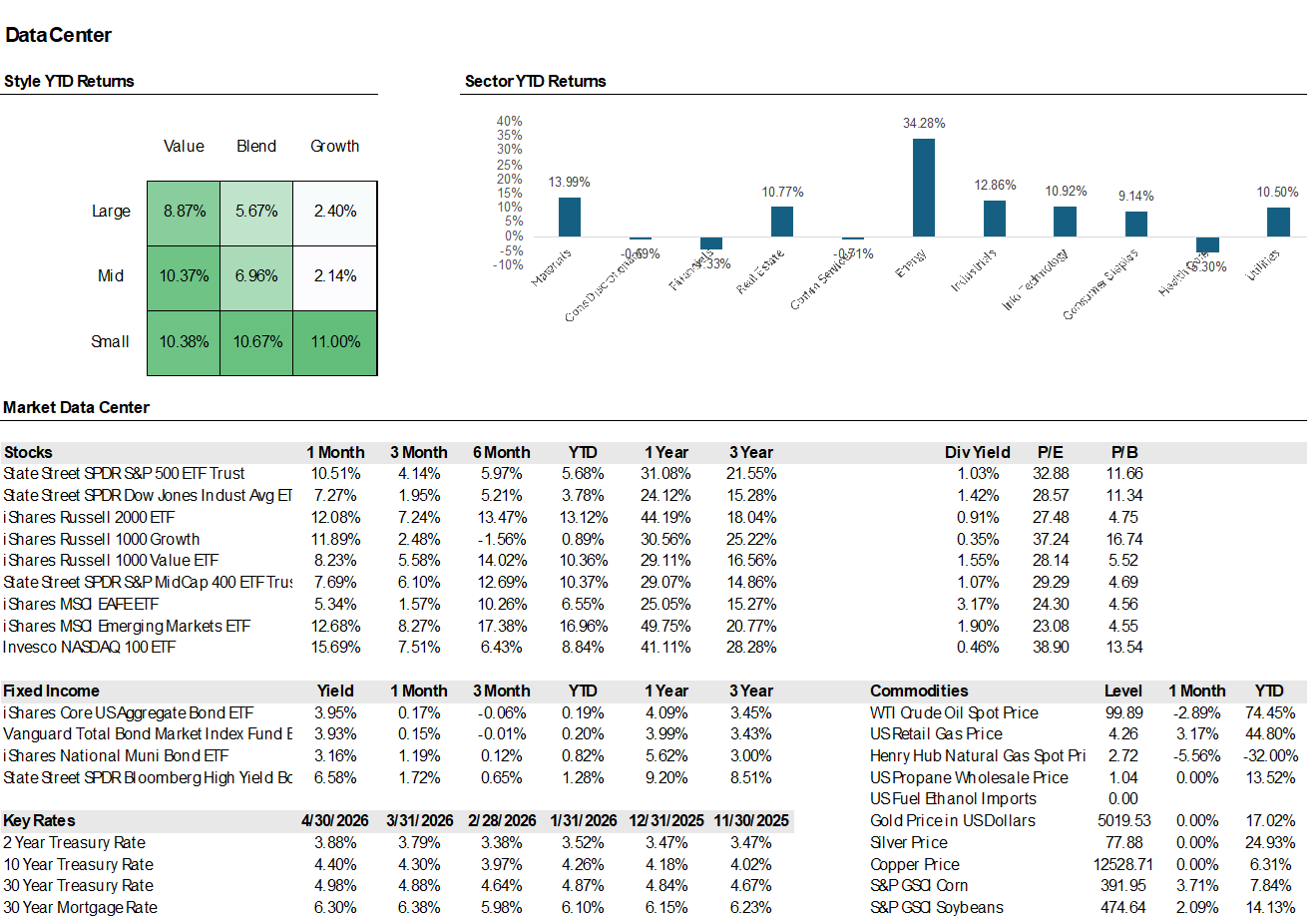

• Best/Worst Sectors: Information Technology led decisively, gaining more than 20 percent as the Magnificent Seven rebounded sharply on stronger-than-expected AI-related earnings. Energy was the only S&P 500 sector to finish April in negative territory, declining approximately 2.6 percent as crude prices pulled back from their March peaks.

• Small-Caps and Mid-Caps: Small-cap stocks, as measured by the Russell 2000 Index, gained approximately 12 percent in April, registering a new closing record on April 24 — the index’s first since January. Mid-cap stocks, represented by the S&P 400 Mid-Cap Index, also participated in the broad rally by rising 7.7 percent.

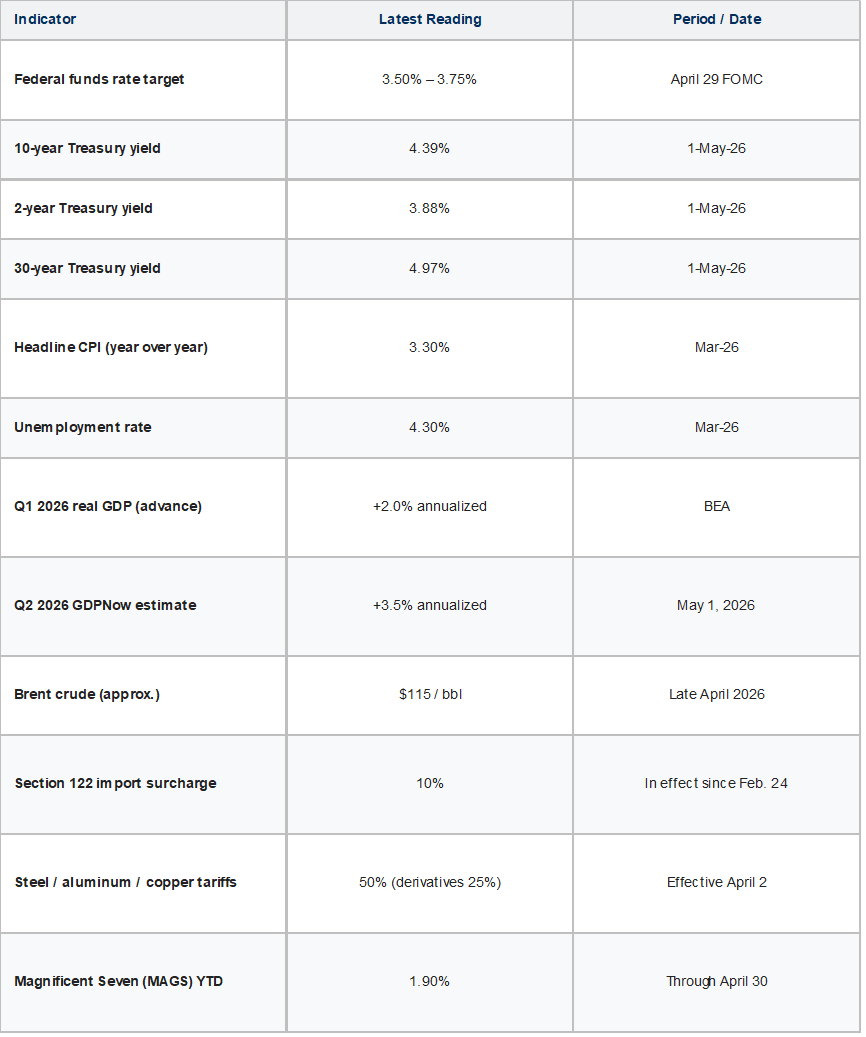

• Bonds: The Bloomberg U.S. Aggregate Bond Index posted a modest return in April as Treasury yields drifted slightly higher. The 10-year Treasury yield ended April near 4.39 percent, up from approximately 4.31 percent on April 10, as the equity rally drained money from duration and the renewed climb in oil prices refocused attention on inflation risk.

• International Developed Markets: The MSCI EAFE Index gained approximately 5.3 percent in April, with year-to-date returns of approximately 6.5 percent. International developed markets continued to participate in the global recovery.

• Emerging Markets: The MSCI Emerging Markets Index reached a record high in April, propelled by technology strength in Korea and Taiwan. The diversification of the AI supply chain across Asia continues to provide a return profile distinct from the U.S. mega-cap names that dominate the headlines.

Key Observations

• The S&P 500’s 10.5 percent gain in April was its best monthly return since November 2020, recovering nearly all of March’s losses and pushing the index to a new closing high on April 24.

• Information Technology led at over 20 percent as Magnificent Seven names rebounded on strong Q1 AI earnings; Energy lagged at -2.6 percent as crude oil prices declined from their peak.

• The Russell 2000 set a new closing record on April 24, its first since January, signaling broader market participation than the mega-cap-only rallies of 2023 to 2025.

• Treasury yields drifted higher; the 10-year ended April near 4.39 percent, pressuring bond returns despite the rally in risk assets.

• International equities continued to participate; MSCI EAFE gained approximately 5.3 percent and MSCI Emerging Markets hit a record high.

• The Federal Reserve held the federal funds rate at 3.50 to 3.75 percent on April 29 in an 8–4 vote — the widest dissent since October 1992.

• The Section 122 ten-percent import surcharge remained in effect; the President’s April 2 proclamation imposed 50 percent tariffs on imported steel, aluminum, and copper, with derivatives at 25 percent.

Market Commentary

Three forces drove April’s recovery. First, the U.S.–Iran ceasefire announced April 8, brokered by Pakistan after roughly forty days of military operations, eased the geopolitical premium that had driven Brent crude to nearly $120 per barrel in March. When Iran’s foreign minister declared the Strait of Hormuz open to commercial shipping on April 17, oil dropped 11 percent in a single session. Second, the Magnificent Seven names that had collectively shed 16 percent in the first quarter staged a forceful rebound, with strong first-quarter earnings from Alphabet, Amazon, Microsoft, and Meta in the final week of April reinforcing the move. Third, market breadth improved meaningfully. The Russell 2000 set a new closing record on April 24, its first since January, signaling that participation extended well beyond mega-cap technology.

Some of the forces that drove March’s decline persist. Iran has at times sought to control Strait of Hormuz traffic and demand tolls on commercial shipping, the U.S. Navy maintains pressure at Iranian ports, and Brent crude climbed back above $114 per barrel by month-end. Energy was the only S&P 500 sector to finish April in negative territory. None of this changes the long-term case for staying invested. Geopolitical and policy uncertainty are constants, not anomalies. The investor’s task is not to predict their resolution but to build a portfolio that can withstand them and keep compounding through them.

International equities continued to participate in the global recovery. The MSCI EAFE Index gained approximately 5.3 percent in April, while the MSCI Emerging Markets Index reached a new record high, propelled by technology strength in Korea and Taiwan. For investors who were tempted to abandon international diversification after years of U.S. mega-cap dominance, the past two quarters have offered a quiet vindication: international equities outperformed U.S. stocks in the first quarter and continued to participate fully in April’s recovery, even as the U.S. rally narrowed the relative year-to-date gap. Diversification is necessary because the future is uncertain. April was simply another reminder.

Bonds were the conspicuous laggard of the month. The 10-year Treasury yield rose to end April near 4.39 percent, with the 30-year near 4.97 percent — both within striking distance of their March highs. Yields rose in part because the equity rally drained money from duration and in part because the renewed climb in oil prices refocused attention on inflation risk. The Bloomberg U.S. Aggregate Bond Index posted a small positive return for the month after a positive first quarter. For balanced portfolios, bonds did exactly what they should have done in the first quarter — cushion the loss in stocks — and exactly what they tend to do in months like April — fail to keep pace with a surging equity market. Both outcomes are features of fixed income, not flaws. Investors who held bonds for the first quarter’s protection should hold them now for the income.

Economic Roundup

Labor Market

The Bureau of Labor Statistics released the March employment report on April 4. Nonfarm payrolls rose by 178,000 — a meaningful improvement from February’s negative print of negative 92,000 and a sign that the labor market did not collapse in the way the headlines of late March suggested. The unemployment rate held essentially steady at 4.3 percent. The April employment report is scheduled for release on May 8 and will be the first comprehensive read on the labor market since the U.S.–Iran ceasefire, the metals tariff escalation on April 2, and the rebound in equities.

Consumer Spending and Inflation

The March CPI report, released April 10, came in firmer than the comparatively soft readings of January and February. Headline inflation rose 0.9 percent month over month and 3.3 percent year over year, both above expectations. The acceleration was substantially driven by energy: the March oil shock fed directly into the index, with gasoline and energy services components rising sharply. Core inflation continued to run above the Fed’s 2 percent target. The April CPI release is scheduled for May 12 and will be the first reading to capture both the temporary energy relief from the April 17 Strait reopening and the new metals tariffs.

Economic Growth

The Bureau of Economic Analysis released its advance estimate of first-quarter 2026 real GDP at 2.0 percent annualized — a respectable result given the geopolitical and tariff disruptions of the period and an improvement from the revised 0.7 percent registered in the fourth quarter of 2025. The Atlanta Fed’s GDPNow model estimated second-quarter growth at 3.5 percent as of May 1, supported by stronger personal consumption and private investment readings. The expected acceleration is partly mechanical, since the first quarter’s weakness gave the second quarter a low base, but the data are sufficient to indicate the U.S. economy continues to experience solid growth.

Federal Reserve Policy

The Federal Open Market Committee voted on April 29 to hold the federal funds rate target range at 3.50 to 3.75 percent — its third consecutive meeting at this level. The decision split the Committee 8 to 4, the widest dissent since October 1992. Three of the four dissenters voted against the decision because they wanted the Committee’s easing bias removed from the statement language. The fourth dissented in favor of a cut. The FOMC statement explicitly cited the Middle East conflict as a source of elevated inflation and economic uncertainty. The April 29 meeting was Chair Jerome Powell’s last as Chair of the Federal Reserve, although he confirmed in the press conference that he intends to remain on the Board of Governors after his term as Chair ends on May 15.

Insights: The Reward for Staying Invested

There is a tendency in financial media to treat every difficult quarter as the start of something worse and every recovery as fragile. The data tell a different story. Across decades of market history, the strongest months tend to follow the worst months, and they tend to arrive without warning. Investors who sold at the March lows missed approximately a 10.5 percent return in the four weeks that followed. There is no reliable way to capture the rebound without enduring the decline. That is why we have consistently said, through every cycle of pessimism, that the long-term investor’s task is to stay invested.

Earnings have supported the recovery in substance, not just sentiment. The first-quarter reporting season is running better than feared. Eight of eleven sectors were reporting year-over-year earnings growth as of late April, led by Information Technology, Materials, Financials, and Industrials. Strong reports from Alphabet, Amazon, Microsoft, and Meta confirmed that the AI investment cycle is producing measurable revenue, not only future promises. Capital expenditure across the Magnificent Seven continues to exceed $200 billion annually, and the market has reaffirmed its judgment that this spending will produce returns. That judgment will be tested each quarter, which is exactly as it should be.

The Federal Reserve’s 8-to-4 dissent at the April meeting is notable for its rarity. Three Committee members wanted the easing bias removed from the statement; one wanted to cut. That spread captures the policy dilemma in real time. A Fed that is internally split is a Fed unlikely to deliver a decisive course change soon, which means rates near 3.50 to 3.75 percent are likely to persist longer than the futures market currently implies. Yields above current and forecasted inflation, available across investment-grade fixed income, represent the most attractive bond environment in nearly two decades.

Tariffs remain a slow-moving structural issue rather than an acute shock. The Section 122 ten-percent surcharge has been in place since February 24 and is currently scheduled to expire under its statutory 150-day limit on or about July 24. The Court of International Trade held a hearing on April 10 to consider its legality. The President’s April 2 proclamation imposed 50 percent tariffs on imported steel, aluminum, and copper, with derivative articles facing 25 percent. The U.S. Trade Representative’s Section 301 investigations against 16 trading partners closed for public comment on April 15. The cumulative effect is a meaningful and rising effective tariff rate for U.S. importers, with multiple legal and statutory deadlines clustered in the third quarter. Long-term investors should expect, not be surprised by, additional headlines through the summer. Headlines have rarely been a reliable basis for portfolio decisions; principles have.

Outlook

April rewarded patience. Investors who held diversified portfolios through March’s worst quarter since 2022 watched April recover nearly all of those losses in four weeks. Investors who sold near the lows missed the strongest single-month rally in nearly six years. This is not a coincidence; it is the consistent pattern of long-term equity returns. The best months follow the worst months, they arrive without warning, and they are nearly impossible to capture from the sidelines. The single most important investment decision most people will ever make is whether to stay invested when staying invested is uncomfortable. April reaffirmed that lesson.

The risks ahead are real and varied. The Iran ceasefire could fray. Tariff policy could shift again. Earnings estimates could be revised lower. The Federal Reserve could disappoint either side of its internal split. None of this is new information, and none of it should drive a reactive change to a long-term plan. Risk is always present in equity markets — it is the reason stocks have historically delivered returns above bonds and cash. The question is not whether risk exists but whether you are being compensated for it and whether your portfolio is built to weather it. For most diversified investors, the answer to both has not changed.

Fixed income deserves a closer look than it has received in years. With the 10-year Treasury yielding 4.39 percent, the 2-year at 3.88 percent, and high-yield credit yielding near 6.7 percent, the income opportunity in bonds is the most attractive in nearly two decades. For investors who have spent three years frustrated by bonds’ inability to keep pace with equities, the opportunity now is the income, not the price appreciation. Locking in yields above current and forecasted inflation is what bonds are supposed to do.

The principles do not change with the calendar. Diversify because the future is uncertain. Time in the market matters more than timing the market. Own quality. Keep costs low. Focus on what you can control. April’s rally and March’s selloff are not opposing data points. They are the same data point, reinforcing the same lesson. Markets reward investors who stay invested. They punish, in lost compounding, those who do not. We said it during the difficult first quarter, and April confirmed it: stay the course.

Sources

Bureau of Economic Analysis (Q1 2026 advance GDP). Bureau of Labor Statistics (March 2026 Employment Situation; March 2026 CPI). Federal Reserve (April 29 FOMC statement and press conference). Federal Reserve Bank of Atlanta (GDPNow Q2 2026 estimate, May 1, 2026). Federal Reserve Bank of St. Louis (FRED Treasury yield series). U.S. Energy Information Administration (Brent crude spot price). Office of the U.S. Trade Representative (Section 301 investigations). The White House (Proclamation 11021, April 2, 2026). U.S. Customs and Border Protection (IEEPA refund processing, Phase 1). FactSet S&P 500 earnings season updates.

Free subscribers: You’ll continue to receive selected articles, market commentary, and educational pieces at no cost.

Paid Substack: ($8/month or $80/year): Get access to subscriber-only posts and occasional featured funds and ETFs.

Founding Member All-Access Bundle: Substack+Website ($179/year): Unlock everything: all paid Substack content plus full access to InvestmentInsights.com, including everything from 90+ in-depth fund and ETF research reports, and member-only resources (model portfolios, Investment Academy and more).

Financial advisors - White-Label Platform ($499/Year): Access the white-label platform at InvestmentInsights.com where you can edit, brand and customize our content designed to save you time and elevate your communication with clients.

Knowledge| Insights | Solutions | Education

Important Disclosures

Copyright © Alan Skrainka, LLC 2026. All rights reserved.

InvestmentInsights.com is owned and operated by Alan Skrainka, LLC. The information on this website and in all published articles is for general informational and educational purposes only and should not be considered personalized investment advice, a recommendation, or a solicitation to buy or sell any security. Neither Alan Skrainka, LLC nor InvestmentInsights.com are registered investment advisors, broker-dealers, or financial planners.

The content published on this site—including article text, charts, podcasts, and reports—has been produced with the assistance of AI tools for data analysis and writing, and is subject to thorough human editorial review. While sources are believed to be reliable and efforts are made to ensure accuracy, completeness and timeliness are not guaranteed.

All model portfolios, mutual fund reviews, and ETF commentaries express the views of the author at the time of publication. Such materials are illustrative, are not tailored to your personal situation, and should not be relied on for investment decisions. Investment decisions should always consider your specific financial situation, risk tolerance, and objectives.

Investing involves risk, including the potential loss of principal. Past performance is not indicative of future results. Securities and ETF values fluctuate and investors may receive more or less than their original investment upon redemption. ETF shares are traded at market prices and may trade at a premium or discount to net asset value. Brokerage commissions and other costs may apply. Diversification does not guarantee profit or protect against loss.

The author may hold personal positions in some of the investments mentioned herein; however, there are no financial arrangements or compensation agreements with any mutual fund company, ETF, or security discussed on this website. Before investing, review the official prospectus and other documents available from the fund provider for important information about objectives, risks, charges, and expenses.

All content is the intellectual property of Alan Skrainka, LLC and may not be reproduced, transmitted, distributed, broadcast, or modified without prior written consent. Unauthorized use is a violation of copyright and other applicable rights and may result in legal action.

All content is provided “as is” without warranty of any kind, and may be changed or updated without notice. InvestmentInsights.com does not provide personalized investment advice or establish a fiduciary relationship. Visitors are strongly encouraged to consult a licensed investment professional before making financial or investment decisions.

This content is intended for U.S. residents only and may not comply with laws or regulations outside the United States.

For questions about this site or to report concerns, please contact us directly.